Strong Brand Strong Business

Playing to win beats playing not to lose

How Lululemon built one of the most commercially precise brands in activewear history on a clear vision and bullish energy — and why losing that clarity is proving expensive

If you work in brand or eCommerce, you’ll know Lululemon. It’s a $10 billion activewear business that went from a single Vancouver store in 2000 to redefining what premium activewear could be — and what it could charge. For a long time it was the best example we had that focusing on a specific customer, and refusing to compromise on that, was a more fruitful commercial strategy than trying to serve everyone.

Nowadays, it’s still used as a case study to prove this point. It’s just that now it’s evidence that the commercials slide when you do make that compromise.

Allow me to elaborate…

Over the past five years, Lululemon’s stock has lost nearly half its value. This is not helped by the fact that its hold on its home market is softening. Which, in turn, isn’t helped by the fact that the brand has shipped the same product quality failure twice in two years.

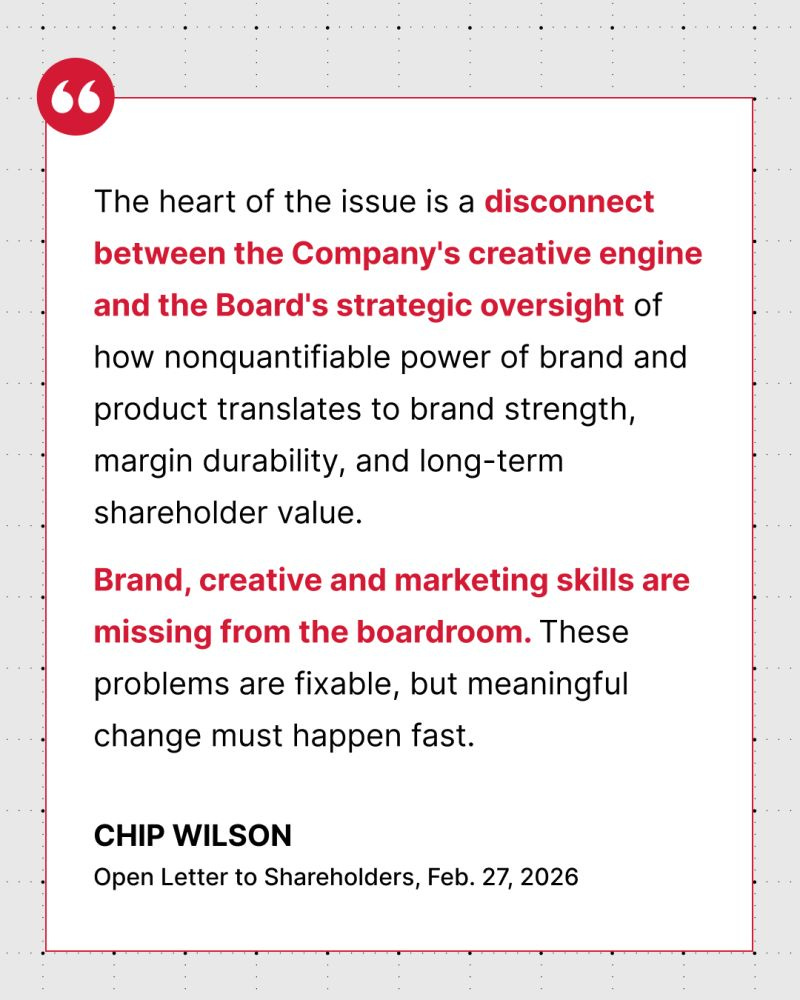

These are big mistakes that have driven Chip Wilson — the founder who built it and departed as chairman in 2013, but still holds more than 9% of the company — to launch a shareholder campaign in early 2026 arguing that the business has lost the plot.

The commercial question that Wilson’s campaign has put back on the table is worth looking at — because when you look at what Lululemon built, what it’s become, and what the brands now outperforming it have in common, the picture is pretty clear.

In this edition of Strong Brand Strong Business, I get into what made the original business work, where the drift started, and what it means for anyone building or scaling a brand-led business right now.

As always, I’d love to hear your thoughts. Find me on LinkedIn and make sure you’re subscribed!

There’s a phrase that keeps cropping up in the Lululemon story. It comes from Wilson himself, writing about the period when he lost control of the company he founded: “I was playing to win, while the directors of the company I founded were playing not to lose. There is a big difference.”

He wrote that in 2018, and he’s making the same argument again in 2026 — this time as a shareholder, not a founder. The company’s own published numbers tell the same story — and the brands eating Lululemon’s lunch right now aren’t doing it by outspending it, but by staying disciplined about who they’re for.

To understand Wilson’s comments and create a benchmark against which to gauge current performance, we need to go back to the founding story.

How did Lululemon become one of the most commercially precise brands in activewear?

Lululemon’s story starts in Vancouver in 1998. Wilson came up with the idea from a yoga mat (where else?!). He was forty-two, had a young family, and by late 2000 had opened the first standalone store. His vision was premium technical women’s activewear, built for yoga but designed for life, sold through community rather than advertising, and — critically — never discounted. The target customer was equally specific: a 32-year-old professional woman Wilson described as “Super Girl.”

Wilson never wanted the brand to speak to every woman. He just wanted it to speak to that woman. This focus was a key part of the brand’s early success. When you know exactly who you’re building for, every decision downstream becomes sharper — from price point and product development through to the store experience and community events. Even through to the “educator model” — a term Wilson insisted on instead of “sales associate” — which turned every store into a physical expression of the brand’s values rather than a transaction point. These were bold calls when you consider that this preceded the rise of eCommerce and the concept store era. But Wilson made them based on a single customer insight that he held with absolute conviction.

By the time Wilson departed as chairman in 2013, Lululemon had revenues approaching $1.6 billion and a gross margin above 55% — the commercial reward for making sure the product was right, the price was right, and the customer felt genuinely seen.

This next bit is where it gets complicated.

What do Lululemon’s recent results actually reveal about the business?

Lululemon’s revenue today is $10.59 billion which no-one can deny is exceptional growth, but it’s hiding the true health of the business. When we look at what’s happening in the markets and pick through the performance metrics, we can make a judgement on whether the commercial engine is structurally sound or beginning to strain.

The most telling signal is the Americas — Lululemon’s home market. In the most recent financial reports, comparable sales decreased 5% year over year, and gross margin fell from 58.5% to 55.6%. While these aren’t big percentages, they’re meaningful when 1% represents $110 million (based on 2025 projections).

It would be remiss not to acknowledge that tariffs are a genuine external headwind — the company estimates tariffs will reduce 2025 operating income by approximately $240 million. I don’t think there’s a single brand strategy that can fully offset a curveball cost of that magnitude. But the home market was softening before tariffs entered the room — and they don’t explain the product decisions that have left the door wide open for competitors to gain ground.

The extra challenge is that this is all happening in public. The stock has shed nearly half its value over the past five years costing shareholders around $20 billion, and there’s been endless coverage around Calvin McDonald stepping down as CEO on January 31, 2026. McDonald was the company’s third CEO transition in recent years, and now the business has CFO Meghan Frank and Chief Commercial Officer André Maestrini serving as interim co-CEOs while Marti Morfitt takes on the role of Executive Chair.

Leadership, top line, bottom line — the instability is everywhere and it’s causing fragility in the business, manifesting as products that don’t live up to customers’ expectations.

Lululemon has a leggings problem — and it signals deep fractures in the business.

In early 2026, Lululemon temporarily pulled its “Get Low” leggings after customers reported they weren’t squat-proof — i.e. they’re see-through when the wearer bends down. The brand put them back on shelves advising customers to buy a size up and wear skin-tone underwear.

Being fair to Lululemon, every brand ships something that doesn’t land. But their response did not align with their entire founding proposition: to provide technically superior activewear, and to respect women’s bodies and their intelligence. What makes this harder to excuse is that it wasn’t the first time — Lululemon pulled its “Breezethrough” leggings for a similar product quality reason in 2024.

A single product failure is a quality control problem. The same failure twice, in the brand’s most fundamental category, tells you something significant about where creative and commercial judgment is operating relative to where the brand was founded. These failures are also leaving the business vulnerable to competitors fulfilling the customer demand that Lululemon is no longer serving.

This week, On announced its Studio Tights — three years in development, tested on hundreds of women across sizes and movement types, with opacity testing built into every stage. On’s senior director of product told Glossy, “We started with the problems”.

A competitor building its entire leggings strategy around the problem Lululemon has now failed to solve twice is not a coincidence.

What does “everything to everybody” actually cost a brand commercially?

McDonald acknowledged that product life cycles had run too long, become too predictable, and caused them to miss opportunities to both create and ride new trends. Yet as much as this presents as a supply chain conversation, this is a problem rooted in poor creative and commercial judgment — the brand had developed systems that worked for the commercials but not for the speed at which creative and product needed to move.

This is what happens when brand, merchandising, and commercial operate as separate departments with different priorities. You end up with a situation where decisions look rational in isolation but they’re damaging in aggregate. So where Lululemon had a supply chain that was optimised for margin, the product didn’t match what customers wanted, so they went elsewhere.

What is Chip Wilson saying about Lululemon? How does he plan to fix the business?

Wilson’s proposed solution is a Brand Product Committee at board level — a governance structure he points to at Amer Sports, where a similar model has helped Arc’teryx and Wilson Tennis outperform the S&P 500 by approximately 89% since its 2024 IPO. Brand judgment with a formal seat at the table, not just a presence in the marketing department — it’s the same argument I made in my previous piece on Adanola, where brand discipline has to permeate the entire business, including its operations. His nominees go to shareholder vote in June 2026.

Marc Maurer — Wilson’s lead board nominee — was Co-CEO of On during exactly this period. The same business now building its leggings strategy explicitly around the problem Lululemon has failed to solve twice.

Why are Alo Yoga and Vuori outperforming Lululemon — and what does it tell us?

Two brands gaining ground in Lululemon’s category are worth examining — because their success is down to them doing the thing Lululemon stopped doing.

Alo Yoga built its brand around a clear generational vision. Its average customer is 28 years old — younger than Lululemon’s core 32-35 demographic — and even though it engages talent like Rosie Huntington-Whiteley (she’s 38) in campaigns, it’s maintained a clean, late-twenties aesthetic with absolute consistency. It grew by being exactly right for the customer it had, drawing new customers in through aspiration rather than by broadening its definition. Alo surpassed $1 billion in annual revenue by 2022 and has maintained a 40%+ growth rate since.

Vuori pursued an entirely different target — men’s athleisure, at a time when the industry was chasing the female shopper. It was founded in a garage in 2015, selling only men’s shorts, going left when everyone else went right delivered profitability every year since 2017 and a $5.5 billion valuation following an $825 million investment in November 2024. Vuori has since added womenswear but this has done nothing to dampen sales. Its average price point is $185 — above Lululemon’s $145 — and the share of Lululemon customers also shopping at Vuori has grown from 1.2% in 2018 to 7.8% by late 2024.

The interesting thing is that neither Alo nor Vuori is trying to be Lululemon. That’s why they work.

Is Lululemon using AI to amplify its vision — or to compensate for losing it?

As a business under commercial pressure, Lululemon is investing significantly in AI — and some of it is working. Ranju Das was appointed as its first Chief AI and Technology Officer in August 2025. Its AI-powered performance marketing work with Google’s Performance Max drove a meaningful reduction in customer acquisition costs, increased new customer revenue, and boosted ROAS by 8%.

Lululemon is also using generative AI to assist with product creation — helping designers move faster. I want to flag this because speed to market as a primary AI objective is a revealing priority…

The problem McDonald identified isn’t speed — it’s judgment. Deploying AI to go faster in the wrong direction doesn’t fix that. It accelerates it. This could prove itself to be a liability when the creative judgment driving it has already lost its precision. After all, the leggings failures didn’t happen because Lululemon moved too slowly. They happened because products that violated the brand’s most fundamental promise reached the market, twice.

What can brand-led businesses take from Lululemon’s story?

Lululemon, Alo, and Vuori each represent a version of the same choice every founder faces at scale: hold the specificity that built you, or loosen it to grow. The ones that held it are outperforming the one that didn’t.

If I could ask you one question about your own business, it’s this:

Are you using AI to amplify a clear commercial vision — or to compensate for not having one defined clearly enough? What you point it at matters more than whether you’re using it. Speed without vision isn’t innovation, and you need to be honest about which one you’re actually chasing.

Researching this piece, it’s obvious that Wilson built something genuinely extraordinary — and for more than a decade, the business was the proof of the brand. But at some point, the game became defensive. It became about protecting market share and position rather than building on it.

That is why playing to win looks different from playing not to lose.

Update: the full year fiscal 2025 results landed on 17th March. Read my signal check here: Lululemon reported $11 billion in revenue. Its home market is still shrinking

Strong Brand Strong Business is part of The Supercharged Mind — published for founders, CMOs, and senior operators in brand-led businesses. Every edition examines a brand building something that lasts — and what the rest of us can learn from how they do it.